Need help paying for

Access lower cost private student loans, exclusively through Juno

- Access the deals below - no cost, no commitment

- Lenders competed for our group's business

- You get the best offer (for your credit profile)

As featured in

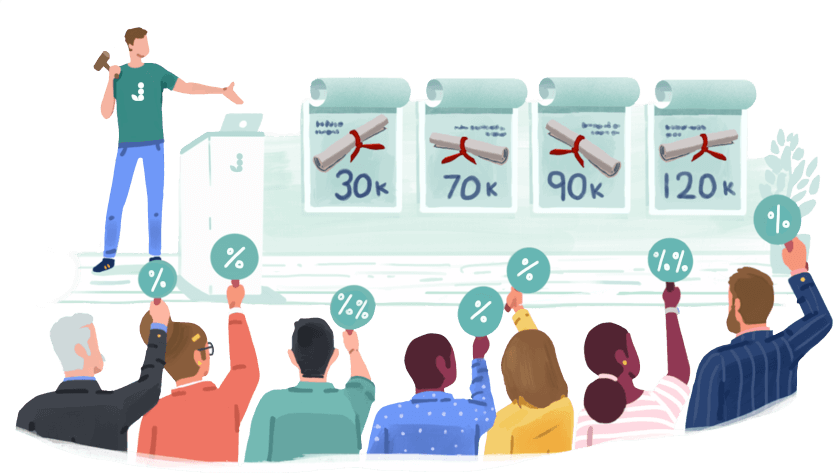

How it Works

We gather large groups of people and get lenders to compete for our business.

ALL YEAR

You sign up.

Tell us a little bit about yourself and help us grow our negotiating power by spreading the word.

EARLY-MAY

We run a bid.

Using the power of your voices, we make lenders compete for our collective business. New Juno members are still welcome during this time!

NOW

We share.

We share the negotiated deals with you and you can decide to use it or not.

There’s no commitment.

Why Juno?

Free, Fast and Easy

Signing up is free and takes less than 2 minutes. We don’t run a credit check and don’t need your social security number.

Better Deals

Months of research and the competitive process ensure that our members get the best rates in the market. You’re always free to compare yourself!

Together

Invite those you care about and help the negotiation be successful. The larger the group, the better our chances of success. You'll also get rewarded for helping grow our community.

Transparent

We will keep you informed through the entire process so you can make informed decisions.

How on earth is this free?

Lenders pay Juno a fee on loans that go through us — that's how we keep Juno free to use for members, at no cost to you. We negotiate with lenders to expand eligibility and lower rates for our members. Learn more about how we make money.

Juno’s Promise

Juno is free for members to use, and we intend to keep it that way. Students, families, and professionals deserve it.

We Are Juno

Recent grads who learned everything you need to know about saving on education costs. We’re always happy to chat, so feel free to send us a note!